Westlake Chemical Partners (WLKP)·Q4 2025 Earnings Summary

Westlake Partners Posts Strong Coverage Ratio as Turnaround Headwinds Fade

February 24, 2026 · by Fintool AI Agent

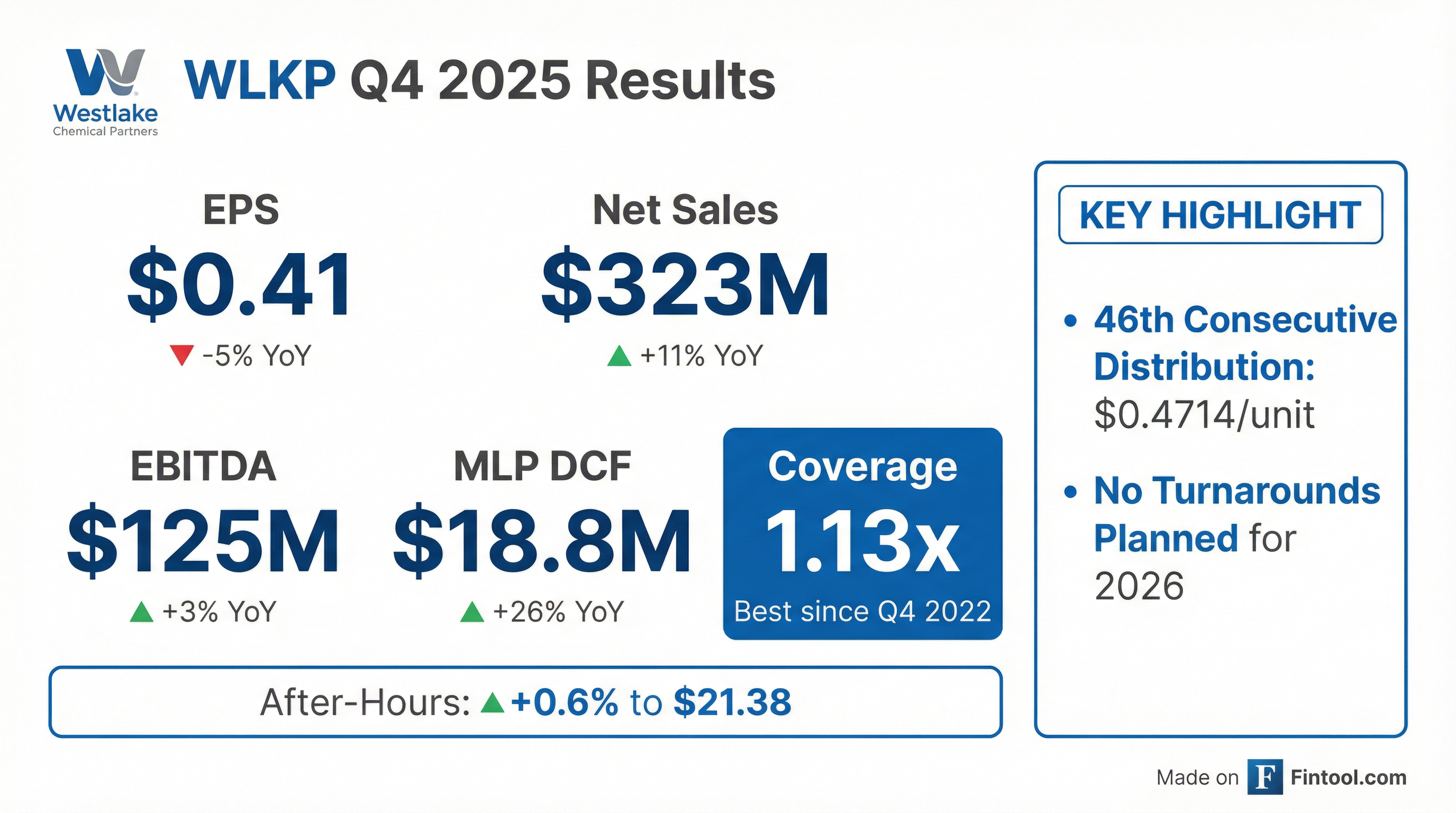

Westlake Chemical Partners LP (WLKP) reported Q4 2025 results with net income of $14.5 million, or $0.41 per limited partner unit, coming in slightly below the prior year's $15.0 million but delivering a coverage ratio of 1.13x—the highest since Q4 2022. The partnership declared its 46th consecutive quarterly distribution of $0.4714 per unit and signaled a stronger 2026 with no turnarounds planned.

Did Westlake Partners Beat Earnings?

WLKP's Q4 2025 EPS of $0.41 missed analyst consensus estimates of approximately $0.45, representing a shortfall of roughly 9%. However, the headline miss obscures several positive developments:

The coverage ratio improvement is the standout metric. At 1.13x, this marks the strongest quarterly coverage since Q4 2022, driven by lower maintenance capital expenditures as spending shifted earlier in the year following the Petro 1 turnaround completion.

How Did the Stock React?

WLKP shares traded up 0.14% during the regular session to close at $21.24, with after-hours trading pushing the stock to $21.38 (+0.6%). The muted reaction suggests the market is focusing on the improving coverage trajectory rather than the modest EPS miss.

52-Week Range: $17.75 - $25.04

Current Yield: ~8.9% ($1.8856 annual distribution / $21.24 price)

The stock has recovered from its 52-week low in mid-2025, which coincided with the Petro 1 turnaround headwinds, but remains well below the 52-week high as higher feedstock costs have pressured margins.

What Did Management Guide?

CEO Jean-Marc Gilson struck an optimistic tone regarding 2026:

"Looking ahead to 2026, the Partnership is positioned for increased production and sales volume with no planned turnarounds following the completion of the Petro 1 turnaround in 2025. We expect the higher production and sales volume to result in improvement in our coverage ratio in 2026, as is typical in years following turnarounds."

Key 2026 Drivers:

- No turnarounds planned — removes the drag that impacted 2025 results

- Higher production volumes expected with Petro 1 fully operational

- Coverage ratio target above 1.1x — CFO confirmed this specific target on the Q&A

- Operating surplus of $74M — "well covers any current or future expected annual distributions"

The ethylene sales agreement with Westlake Corporation continues to provide 95% of OpCo's production at a fixed $0.10/lb margin, ensuring predictable cash flows despite global petrochemical volatility.

What Changed From Last Quarter?

Q4 2025 marked a return to normalized operations after the turnaround-impacted first half of the year:

The significant improvement in distributable cash flow and coverage ratio reflects lower maintenance capex as spending normalized post-turnaround, along with favorable working capital changes.

Full Year 2025 Performance

The Petro 1 turnaround weighed heavily on full-year results:

The trailing twelve-month coverage ratio stood at 0.80x at quarter-end, up from 0.75x at Q3 2025. This remains below 1.0x due to the turnaround impact but is trending toward normalization.

Capital Structure and Distribution

WLKP maintains a conservative balance sheet with $400M in long-term debt payable to Westlake Corporation.

Balance Sheet Highlights (Dec 31, 2025):

- Cash and equivalents: $44.3M

- Total assets: $1.26B

- Total equity: $802.4M

- Long-term debt to Westlake: $399.7M

The partnership's fee-based structure under the ethylene sales agreement with Westlake Corporation provides stable cash flows regardless of ethylene price volatility. This structure has delivered distributions through "economic ups and downs, as well as planned and unplanned turnarounds" for over 10 years since the IPO.

Q&A Highlights

On Distribution Sustainability and Operating Surplus:

Analyst James Allshull questioned whether the partnership had to draw down on its Investment Management Agreement balance to fund distributions. CFO Steve Bender explained the mechanics:

"The operating reserves in 2025 were strong enough that we had strong enough balances in that operating reserve to continue to pay distributions. When you think about the operating surplus we had at the end of 2025, it was approximately $74 million. That well covers any current or actually future expected annual distributions by the partnership."

The CFO confirmed that with no planned turnarounds in 2026, coverage ratio should rise above the 1.1x target, and operating surplus and investment balances will rebuild.

On Growth Financing:

When asked how potential acquisitions or OpCo ownership increases would be funded, management outlined a "drop-down" strategy:

"Should we decide to undertake any of those growth opportunities, we would undertake what we'd characterize as a drop-down, where a party would monetize a portion of OpCo interest and contribute that down, and we would finance that with external funding, whether it be debt or equity or some combination."

This provides a clear roadmap for the partnership's four growth levers: increased OpCo ownership, qualified income stream acquisitions, organic expansions, and Ethylene Sales Agreement margin renegotiation.

Risks and Considerations

Near-term headwinds:

- Higher feedstock costs: Ethane and natural gas costs increased 47% and 45% YoY in Q3 2025

- Soft industrial demand: Global manufacturing weakness continues to impact the chemical industry

- Below-1.0x trailing coverage: Despite Q4 improvement, TTM coverage at 0.80x suggests distributions exceeded cash generation in 2025

Structural supports:

- Take-or-pay contract: 95% of production sold to Westlake at fixed $0.10/lb margin

- Agreement renewals: Ethylene Sales Agreement and Feedstock Supply Agreement renewed through December 2027

- No near-term turnarounds: 2026 production should be uninterrupted

Key Takeaways

- EPS missed by ~9%, but MLP distributable cash flow jumped 26% YoY

- 1.13x coverage ratio is the highest since Q4 2022, signaling turnaround headwinds are fading

- 46th consecutive distribution maintained at $0.4714/unit (~8.9% yield)

- No 2026 turnarounds planned, positioning the partnership for improved cash generation

- Feedstock costs remain elevated, but fee-based structure provides margin protection

View the full Q4 2025 Earnings Release or explore WLKP's company profile.